When Info Edge‘s board approved a ₹39.91 crore buyout of the remaining 45.36% stake in Coding Ninjas on July 6, most coverage treated it as a routine cap-table cleanup — a company that had backed an edtech platform since 2020 finally taking full ownership. That framing undersells what the deal actually is: the fourth time in six years Info Edge has converted a startup bet into a wholly owned subsidiary, and a useful marker for how differently Indian edtech companies are being absorbed, rescued, or wound down as the sector’s post-pandemic reckoning runs its course.

Info Edge’s ownership playbook has a consistent shape, even when the entry points differ. With Zwayam, an AI-powered recruitment software company, Info Edge went straight for 100% ownership in 2021, paying roughly ₹61 crore ($8.3 million) to bring it in as a full subsidiary within weeks of announcing the deal. DoSelect (operated by Axilly Labs) was folded in the same year through a similar direct buyout. Highorbit Careers, the parent of recruitment platforms iimjobs and hirist, was acquired outright in FY2019-20. In each of these cases, Info Edge skipped the minority-stake phase entirely — it bought the whole business in one motion because the target filled a specific gap next to Naukri.com’s core recruitment business.

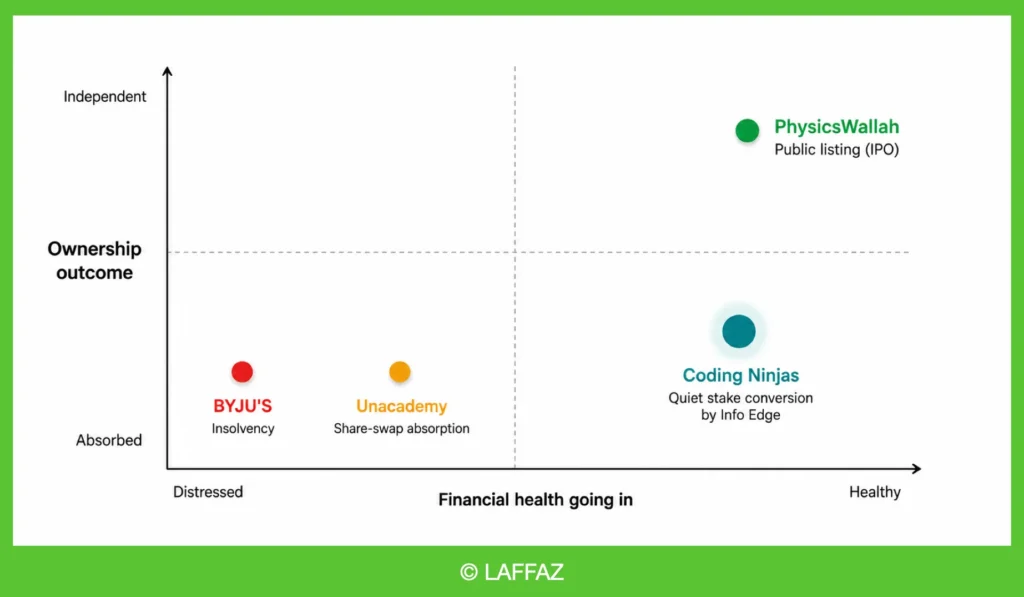

Coding Ninjas followed a different arc, and that difference is the more interesting part of the story. Info Edge first backed the coding-education platform’s Series A round in 2020, then increased its holding to a majority stake through follow-on transactions in 2022, before this month’s deal closed out the remaining minority position. The payment itself is structured in deferred tranches — 25% at closing, the rest spread across three annual instalments through 2029 — a structure that lets Info Edge complete full ownership without a large upfront cash outlay. That’s a meaningfully different signal than the Zwayam-style instant buyout: it reads less like an urgent acquisition and more like a company converting a long-held minority position into full control once it had enough confidence in the unit economics to justify the balance-sheet commitment.

And the underlying numbers support that reading. Coding Ninjas isn’t a distressed asset being absorbed to prevent a collapse. Its revenue grew from roughly ₹53 crore in FY24 to about ₹67 crore in FY25 and nearly ₹97 crore in FY26, with losses narrowing over the same period. This is a company on an improving trajectory, not one that needed rescuing, which makes the full-ownership move look more like portfolio tidiness than crisis management. Info Edge gets direct control over integrating Coding Ninjas’ course catalogue with Naukri’s broader upskilling push, without managing that integration through a shared cap table.

That distinction matters because it sits in sharp contrast to what’s happening elsewhere in Indian edtech right now. The sector’s most consequential deal this year was upGrad‘s acquisition of Unacademy through an all-stock, share-swap transaction announced in March 2026 — a deal widely read as signalling that India’s edtech story has entered a consolidation phase rather than continuing its pandemic-era expansion. Unlike Coding Ninjas, Unacademy wasn’t a healthy business quietly converting a stake — its valuation had fallen more than 85% from a 2021 peak of $3.5 billion to under $500 million, and the deal arrived after the company disclosed roughly $100 million in cash reserves following a year of consolidating company-run centres with franchise partners. Unacademy co-founder Gaurav Munjal acknowledged as much publicly, writing that the company had “lost some focus and market share” and that the sector itself “has not seen enough real product innovation in recent years.”

At the harsher end of the same spectrum sits BYJU’S, whose collapse from a $22 billion valuation into insolvency proceedings remains the sector’s starkest cautionary tale — a case study in what happens when aggressive acquisition-fuelled growth outruns the underlying unit economics. Investors, including Prosus and BlackRock, eventually wrote their stakes down to zero.

Set against those two, PhysicsWallah represents a third and very different path: it stayed disciplined through the funding winter, turned profitable, and completed a public listing in November 2025 at a premium to its issue price — proof that at least one large edtech player found a way to scale without needing either a rescue acquisition or a distressed sale.

Read together, these four situations — Info Edge/Coding Ninjas, upGrad/Unacademy, BYJU’S, and PhysicsWallah — sketch out the range of exits now available to Indian edtech companies as the sector matures past its 2021 boom. A founder with a fundamentally sound but sub-scale business, sitting inside a larger diversified parent that already holds a majority stake, can convert into a wholly owned subsidiary on favourable, deferred terms — a comparatively quiet, founder-friendly landing. A founder whose valuation has collapsed but who retains a meaningful market position can find a strategic buyer willing to absorb the business via a share swap, trading independence for survival. A founder who badly overextends on acquisition-led growth without matching fundamentals risks the BYJU’S outcome. And a small number of disciplined operators will simply out-execute the correction entirely and go public on their own terms.

What the Coding Ninjas deal specifically demonstrates is that full-ownership consolidation doesn’t have to mean distress. Info Edge has now run this playbook four times, and the through-line across Zwayam, DoSelect, Highorbit Careers, and Coding Ninjas is control over adjacent capabilities that reinforce Naukri’s and its portfolio’s core businesses, executed at a pace and structure that suits Info Edge’s own balance sheet rather than any external pressure on the target. That’s a meaningfully different kind of consolidation than the one reshaping the rest of India’s edtech sector — and one worth watching as more Info Edge-backed minority stakes mature toward similar decisions in the coming years.